Consultation on ATAD 2 (reverse hybrids) and amendment arm’s-length principle in the Netherlands

As noted in our earlier Tax Alerts (see our Tax Alerts of March 2017 and July 2019), the EU Anti-Tax Avoidance Directive 2 ("ATAD 2") provides for minimum standards to neutralize hybrid mismatches and came into effect in the Netherlands as of 1 January 2020. However, as an exception, the rule that targets so-called “reverse-hybrid” mismatches will become effective only as of 1 January 2022.

The Dutch government has released a consultation document (the “Consultation Document”) on 4 March 2021 containing a draft bill of law and explanatory memorandum targeting reverse-hybrid mismatches in order to garner feedback from interested parties. Simultaneously, the Dutch government has released a consultation document on targeting mismatches resulting from the application of the arm’s-length principle (notably, the abolishment of the ‘informal capital’ doctrine). Comments can be submitted until 2 April 2021.

Reverse-hybrid measure

A reverse hybrid entity is an entity (generally a partnership) that for tax purposes is considered transparent in its jurisdiction of incorporation/establishment, whereas the jurisdiction of one or more related participants qualifies the entity as non-transparent. A participant is considered ‘related’ if it holds a direct or indirect interest of 50% or more of the voting rights, capital interest or profit rights in the entity. In short, the reverse-hybrid measure aims to tackle the hybrid mismatch at the source by making the hybrid entity subject to tax. Effectively, a reverse hybrid entity will become subject to Dutch corporate income tax only to the extent that the profit is attributable to related participants that qualify the entity as non-transparent. Similarly, distributions by a reverse hybrid entity will only become subject to Dutch dividend withholding tax (dividends) and the new Dutch conditional withholding tax (interest and royalties) to the extent the distribution is attributable to related participants that qualify the entity as non-transparent.

As an exception, the reverse-hybrid rule will not apply to regulated collective investment vehicles with a diversified portfolio.

Structures likely to be affected

The reverse-hybrid rule is likely to affect Dutch transparent CV's (i.e. limited partnerships) used in a CV-BV structure, where the CV is considered to be transparent for Dutch tax purposes and related non-resident participants are located in a jurisdiction that view the CV as non-transparent (e.g. under the US check-the-box regime). Income received at the level of the CV (e.g. interest or royalty payments made by a Dutch BV) would not be subject to tax in the Netherlands as a result of the CVs transparent nature. This non-inclusion of interest or royalty income has already been tackled by the existing ‘regular’ neutralizing ATAD 2 rules.

Additionally, as of 1 January 2022 the reverse-hybrid rule will apply at the level of the CV as a result of which the CV is deemed to be a Dutch tax resident and its income may be subject to Dutch taxation. As the reverse-hybrid rule tackles the discrepancy between qualifications in different jurisdictions (i.e. the cause of the mismatch), in these types of situations the reverse-hybrid rule renders the regular hybrid mismatch rules obsolete.

The Consultation Document provides the following illustrative examples:

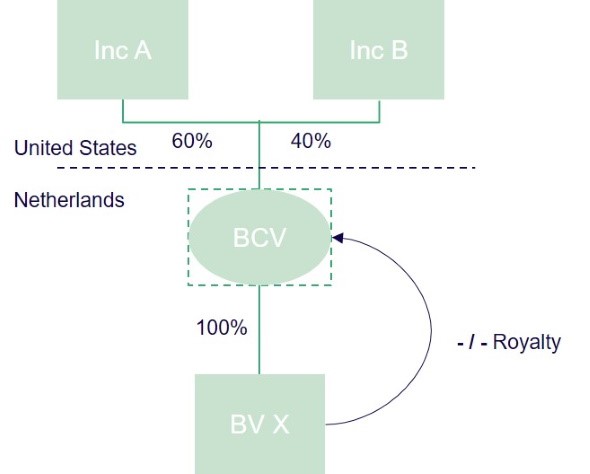

Example I

In this example B CV is transparent from a Dutch tax perspective which leads to allocation of its profits to B CV’s investors.

Both investors – Inc A and Inc B – are located in the US. B CV is viewed as non-transparent from a US tax perspective which results in Inc A and Inc B not being allocated any of the profits of B CV. B CV is not taxed in the US .

Under the regular hybrid mismatch rules royalty payments made my BV X to B CV lead to a non-deduction of the royalty payments at the level of BV X.

Under the reverse-hybrid rules B CV is viewed as non-transparent from a Dutch tax perspective and therefore taxable in the Netherlands for all of its profits (the royalty payments by BV X should in principle be deductible as B CV’s profits will be subject to tax).

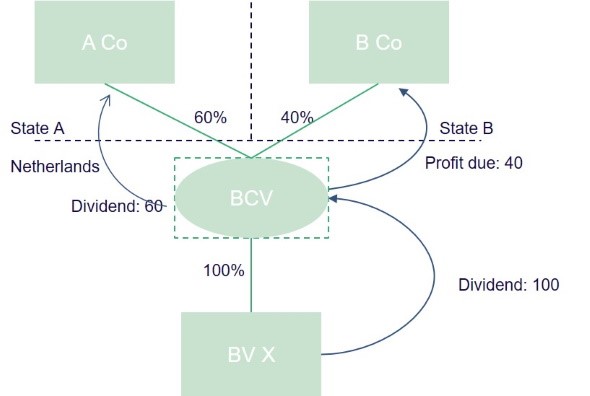

Example II

General remarks

B CV is transparent from a Dutch tax perspective which leads to allocation of its profits to B CV’s investors.

State A views B CV as non-transparent for taxation purposes and as such does not allocate B CV’s profits to A Co, but to B CV.

State B views B CV as transparent for taxation purposes which results in State B allocating its profits to B Co.

As A Co is entitled to at least 50% of the profits of B CV (60%) and State A deems B CV non-transparent for taxation purposes, B CV would qualify as a reverse-hybrid under the reverse-hybrid rules and subsequently be subject to taxation in the Netherlands (to the extent that B CV’s income of 60 is not picked up in State A).

State A – contrary to State B (also not a Member State of the EU or EEA) – is party to a tax treaty with the Netherlands which contains a dividend provision.

Distribution by BV X to B CV

B CV receives a dividend amounting to 100 – which dividend is exempt at the level of B CV due to the participation exemption – from BV X. Under the proposed reverse-hybrid rules B CV qualifies as the beneficiary of dividends distributed by BV X. In principle the dividend distribution is covered by the dividend withholding tax exemption. However, this exemption is not applicable if the investors in the reverse-hybrid were to hold the shares in BV X directly and if in that scenario the dividend withholding tax exemption would not apply. The distribution made to B Co would be subject to dividend withholding tax as State B (non-Member State of EU/EEA) has not concluded a tax treaty – including a dividend provision – with the Netherlands and therefore does not meet the requirements of the dividend withholding tax exemption.

This results in the following Dutch tax treatment of the dividend distribution made by BV X to B CV:

- distribution in the amount of 60: exempt from Dutch dividend withholding tax; and

- distribution in the amount of 40: subject to Dutch dividend withholding tax.

Distributions by B CV to A Co and B Co

The distribution to A Co in principle would be subject to Dutch dividend withholding tax under the reverse-hybrid rules, as State A views B CV as non-transparent for taxation purposes. However, as A Co is located in a jurisdiction with whom the Netherlands has concluded a tax treaty which contains a dividend provision, this distribution may be exempt from dividend withholding tax.

As B CV is viewed as transparent for taxation purposes by State B, B CV does not qualify as withholding agent in respect of the distribution to B Co. Additionally, B Co is not deemed to receive a dividend distribution under the reverse-hybrid rules due to B Co’s profit rights not being equated to a shareholding.

Amendment arm’s-length principle

Under the current Dutch interpretation of the at arm’s length principle, at arm’s length expenses are in principle deductible, regardless of whether the corresponding income is recognized and/or taxed at the level of the recipient (the so-called informal capital doctrine).

The Consultation Document aims to render the arm’s-length principle ineffective in cross-border situations to the extent that it leads to reduced profits in the Netherlands without a corresponding inclusion in the counterparty’s jurisdiction (a minimum tax rate on the amount of the upward adjustment is unspecified). The measure also targets deductions of the same costs by Dutch tax residents and related parties in other jurisdictions. The measure would essentially apply to downward adjustments associated with increased expenses, reduced revenue, or increased value of assets acquired from a related party. In short the legislative proposal prevents adjustments leading to double non-taxation. The intended entry into force of the legislative proposal is 1 January 2022.

Summary

The legislative proposals up for consultation are the latest measures taken by the Netherlands as further implementation of ATAD2. The proposed amendments target reverse hybrids and application of the arm’s-length principle leading to ‘harmful’ tax practices.

The internet consultation closes on 2 April 2021. We will keep you informed of further developments.