Introduction of dividend withholding tax in relation to low tax jurisdictions as per 2024 and update Dutch double tax treaty policy

1. Proposal to introduce dividend withholding tax in relation to low tax jurisdictions as per 2024

The first letter dated 29 May 2020 contains an announcement of a new withholding tax on dividends to low tax jurisdictions (the ‘letter’). In addition to the conditional withholding tax on interest and royalty payments, which will enter into effect as of 1 January 2021 (see our Tax Alert of 18 September 2019), the Dutch government proposes the new withholding tax on dividends to low tax jurisdictions in an effort to discourage tax avoidance and profit shifting. Dividend distributions to low tax jurisdictions (‘LTJs’) with whom the Netherlands has not concluded a double tax treaty are already subject to dividend withholding tax. New anti-abuse rules were introduced as per 1 January 2018. However certain intra group tax exempt dividend distributions to LTJs are still possible. The current proposal intends to tackle these remaining tax-exempt dividend distributions.

As to its background, in September 2018, the Dutch government published a legislative proposal regarding the abolition of the Dutch dividend withholding tax (‘DWT’) and the introduction of a conditional withholding tax on dividends, interest and royalty payments to LTJs and in abusive situations. At the time, the Dutch government decided to maintain the DWT and to postpone a conditional withholding tax on dividends (see our Tax Alerts of 20 September 2018 and 16 October 2018). The Dutch government now plans to introduce a new withholding tax on dividends to LTJs as of 1 January 2024.

Low tax jurisdictions

Dutch tax law already includes the concept of LTJs for CFC-regime purposes (see our Tax Alert of 18 September 2019). Currently, the following jurisdictions qualify as a LTJ: (i) based on a statutory profit rate lower than 9%: Anguilla, Bahamas, Bahrain, Barbados, Bermuda, British Virgin Islands, Cayman Islands, Guernsey, Isle of Man, Jersey, Turkmenistan, Turks and Caicos Islands, United Arab Emirates and Vanuatu; and (ii) based on the EU-list of non-cooperative jurisdictions for tax purposes: American Samoa, Fiji, Guam, Oman, Samoa, Trinidad and Tobago, US Virgin Islands and Vanuatu.

The Dutch State Secretary of Finance indicated in the letter that the Dutch government has the intention to devise the measures of the new withholding tax on dividends to LTJs before the end of the current Dutch government’s term of office (i.e. March 2021). It is envisaged to introduce the new withholding tax on dividends to LTJs as per 1 January 2024.

2. Update Dutch double tax treaty policy

Introduction

The Dutch State Secretary of Finance, after public consultation, had sent a memorandum (the ‘Memorandum’) dated 29 May 2020 that includes the updated Dutch double tax treaty policy to the Dutch parliament. This policy outlines the positions of the Dutch government when entering into a double tax treaty (‘DTT’). The previous memorandum from 2011 was outdated, mainly as it preceded the OECD Base Erosion and Profit Shifting (‘BEPS’) project and only to a lesser extent took into account the special position of developing countries. As to BEPS, the positions included in the latest update are basically in line with the positions the Netherlands took upon signing and ratifying the ‘Multilateral instrument to implement tax treaty related measures to prevent base erosion and profit shifting’ (‘MLI’).

Key elements of Dutch double tax treaty policy

The Netherlands enters into DTTs to stimulate economic growth by mitigating double taxation. Given that the Netherlands is an open economy with a relatively small domestic market, a large treaty network is economically important for the Netherlands. As a starting point, the Netherlands is therefore open to entering into a DTT with any state, although in practice the nature and size of economic relations are important considerations for entering into a DTT (See however below the section ‘Tax treaties with specific groups of countries’).

A key policy aspect to the Dutch government is that DTTs should not be abused. For this purpose it has not only endorsed the minimum standards agreed in the BEPS-project, but also accorded most other anti-abuse measures for DTTs proposed in the BEPS reports. In this respect DTTs should not impede the application of anti-abuse rules stemming from EU-rules (e.g. ATAD1 and ATAD2. See also our Tax Alerts of 20 September 2018, 16 November 2018 and 9 July 2019 respectively).

Furthermore, DTTs should support a competitive Dutch business climate, which leads the Dutch government to taking into account the benefits included in DTTs of other (West European) states. Given the relatively small Dutch domestic market, it is longstanding tax treaty policy that Dutch enterprises and employees can compete on an equal footing with foreign local enterprises and employees (i.e. capital import neutrality). Whether this position will have to be amended following the outcome of the international debate on the international allocation of business profits and minimum taxation (which the Netherlands on itself supports) remains to be seen.

When entering into tax treaty negotiations, the OECD Model Tax Convention is the starting point for the Netherlands. For treaty negotiations with developing countries the UN Model Tax Convention is increasingly important. In respect of the latter, the Netherlands is open to accepting UN Model Tax Convention provisions (generally providing more taxing rights to source states) more often than before. The Netherlands also aims at including a general provision in DTTs that acknowledges the importance of the OECD commentary for the interpretation of DTTs.

Addressing abuse of DTTs

Upon the release of the final BEPS reports in October 2015, The Dutch government approved of the large majority of measures proposed in the reports. With respect to DTTs all substantive provisions included in the MLI were embraced (and going forward considered part of the DTT policy), except for the general savings clause (included in article 11 of the MLI and to which a full reservation was made).

Minimum standards

The Netherlands, being a member of the Inclusive Framework, commits to the minimum standards agreed in the BEPS project. Regarding BEPS Action 6 that addresses the abuse of DTTs, it prefers meeting the minimum standards through the MLI. States that are not a party to the MLI and with whom the Netherlands has concluded a DTT that carry a substantial risk of treaty abuse, will be approached to amend the DTT in order to meet the minimum standards. No DTT will be concluded if parties cannot agree on meeting the minimum standards.

The Netherlands has a preference to meet the minimum standard by including the principal purpose test (‘PPT’) in its DTTs, as it provides the flexibility to counter abuse of tax treaties without harming real business activities. Upon including the PPT in DTTs the Dutch government also aims at including two complementing provisions. The first provision entails that, to the extent that treaty benefits that would have been granted in absence of the construction/transaction, can still be granted upon request of the taxpayer concerned. The second provision entails that the state that intends to apply the PPT (not granting DTT benefits) must consult the other contracting state regarding its intention to deny treaty benefits. The alternative minimum standard whereby the PPT is complemented by a (simplified) limitation on benefits (‘LoB’) is not favoured by the Netherlands although it is open to accepting it if a treaty partner requires a LoB provision to address treaty abuse. The Netherlands is reluctant in accepting the alternative minimum standard consisting of a detailed LoB complemented by an anti-conduit provision.

Additional anti-abuse measures

As mentioned the Netherlands also accords to the other measures included in BEPS project in relation to the abuse of DTTs (Articles 8 -15 of the MLI), with the exception of a general savings clause. With respect to the latter the Netherlands, for example, favours to include in its DTTs, an anti-hybrid entity provision that includes a specific saving clause that is required to enable the Netherlands to tax entities that are located in the Netherlands but are considered tax transparent by the other contracting state. With respect to BEPS action 7 (Articles 12-15 of the MLI), which addresses the artificial avoidance of a permanent establishment, the Netherlands has made a reservation to article 12 of the MLI. Art. 12 addresses so-called commissionaire structures and amends the permanent representative definition as included in article 5 of the OECD Model Tax Convention. This reservation may be revoked once proper dispute resolution mechanisms are in place.

With respect to mutual agreement procedures, the Netherlands aims at including a provision in DTT”s that allow the authorities to make arrangements regarding interest, penalties and costs in relation to adjustments under mutual agreement procedures.

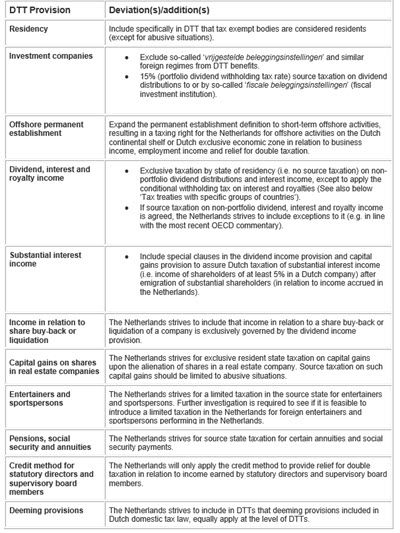

Deviations from and additions to the OECD Model Convention

The Netherlands generally adheres to the OECD Model Tax Convention. A limited number of deviations and additions occur. Below we will briefly address the main deviations and additions.

Click to enlarge.

Tax treaties with specific groups of countries (developing countries, non-cooperative/low tax jurisdictions and neighboring countries)

The Netherlands supports developing countries in levying their taxes. This is reflected amongst others during the process of negotiating tax treaties with these countries. In this respect the Netherlands aims to include general and specific anti-abuse provisions in the tax treaties with developing countries, as a result of which the right to levy taxes for such countries is generally better protected. In addition, the special position of these countries is a justification for the Netherlands to include parts of the UN Model Tax Convention in the relevant DTTs. For example, the Netherlands is prepared to accept a more extensive definition of permanent establishments. Notably a so-called ‘services permanent establishment’ will be included in the relevant tax treaties; also the Netherlands is willing to include a source taxation for technical services when performed in a developing country. The Netherlands is reluctant to agree to a limited source taxation on profits realized in the shipping and air travel industries. Furthermore, in relation to developing countries the Netherlands is willing to agree to somewhat higher withholding taxes on dividends, interest and royalties. Lastly, the Netherlands will continue to provide technical support in order to improve the capacity of the tax authorities in the developing countries.

The Netherlands indicates that it will not enter into tax treaties with countries that are considered non-cooperative by the European Union based on the agreed standards, which relate amongst others to transparency and harmful tax competition. On the other hand, the Netherlands is willing to enter into tax treaties with countries that are considered LTJs (see also part 1 above), but this has no priority as the risk of double taxation should generally be limited. In order to discourage the use of the Netherlands as a conduit jurisdiction, the Netherlands will start levying a withholding tax on interest and royalties at an expected rate of 21.7% in intra-group (and abusive) situations when payments are made directly or indirectly to residents (or permanent establishments) located in non-cooperative or low tax jurisdictions. The Netherlands will aim to amend existing DTTs with such jurisdictions (or potentially terminate in case of a non-cooperative jurisdiction) with a view to effectively levying withholding taxes on interest and royalties (and dividends) made to these jurisdictions. Depending on the facts and circumstances, exceptions (i.e. reduced rates or a 0% rate) may be introduced in order not to affect genuine business activities performed in these jurisdictions.

Also the Dutch government confirms that it will continue to limit tax barriers for frontier workers in order to stimulate the economy in the border areas. This is in particular relevant in relation to the tax treaties with the neighboring countries Belgium and Germany.